Demand for grasses and clovers continues to increase across Europe and around the globe

Faultless service in the face of global disruption has been the DLF theme of the past year. Covid-19, container shortages, rising demand, low stocks from the previous year, and below-average harvests have raised prices for the third year in a row. Our analysis of the market and the factors that will influence price and availability for the coming year are a must-read.

15/06/2021

A below-average harvest for crop 2020 failed to rebuild stock levels

We moved fast in the summer of 2020. As soon as the July harvest was in, we began shipping grass and clover seed and consumer turf mixtures to the near-empty warehouses of our distribution partners. Their experience of the previous year had persuaded them to order more seed – and to order it earlier – to be ready for another good spring season in 2021.

The harvest yield was below normal in Denmark, and far below in The Netherlands. This poor result coincided with an increase in demand within the consumer turf segment driven by consumers spending time at home during the pandemic. After a nervous spring 2020 in the professional turf segment that lowered the activity, the segment recovered slowly through sod production and single outdoor sports activities such as golf. The forage segment returned to normal consumption after recovering from the drought and mice damage of the previous two years. Nevertheless, the top varieties of many forage species had already sold out by Christmas 2020. The situation was similar for the turf segment, with almost no availability across species and varieties.

Shortages drove prices higher

A huge worldwide demand for grass and clover seed boosted market prices. The situation was made more complicated by a shortage of containers for shipping seed around the world. The pressure on European homegrown seed was intensified by fewer exports from overseas suppliers, especially from North America and New Zealand. The result was a significant increase in prices for the third year in a row. Increased demand from China also added to market pressures. Our expectation now is for very low levels of stock at the end of our financial year, 30th June 2021.

TURF: Mixture sales broke capacity record at DLF facilities

The demand for consumer turf remained high at do-it-yourself stores, garden centres, supermarkets and discounters. Online sales gained market share. Consumer demand continued to be driven by the number of people working from home throughout Europe during the pandemic.

Data from several European countries confirm very good sales in the gardening segment. For instance the UK Garden Centre Association’s Barometer of Trade Stats reports record turnover in garden centres and many new gardeners. In Germany, IFH retail reported a steep growth in gardening, including e-commerce sales. And the Dutch market research bureau, GFK, recorded double-digit growth in gardening sales.

The impact of the low-to-zero carry-over from the 2019 crop combined with a very poor 2020 yield, in quantity and quality, for all sub-species of red fescues has altered the way we make up standard mixtures. We mostly replaced the shares of slender, chewing and creeping fescues with smooth-stalked meadow grass. This species recovered pricewise from a small dip, caused by some irregularities overseas, that has increased usage in mixtures. Perennial ryegrasses, which have been in demand across the world (North America and China as well as Europe), sold out several months ago.

In particular, our tetraploid 4turf® varieties are gaining market share in the professional turf sector: the European Seed Journal recently nominated our high-performing 4turf variety FABIAN as one of the most innovative plant varieties of 2020.

In particular, our tetraploid 4turf® varieties are gaining market share in the professional turf sector: the European Seed Journal recently nominated our high-performing 4turf variety FABIAN as one of the most innovative plant varieties of 2020.

Prices for tall fescues are also firming up, driven by a lower-than-expected harvest, fewer imports from overseas and by a shortage of red fescues. The professional turf segment is recovering from the ban on outdoor sports activities. One positive outcome of this is an increased demand for the DLF Select programme for golf courses and sod production.

FORAGE: Spring demand remained on an average level

Spring consumption was generally at normal levels. The peak demand experienced over the past two years was not repeated. But the low inventory from the 2019 crop and 2020’s bad harvest mean that there will be not much oversupply by the end of June. The top varieties were in particular demand and sold out early.

Recommended varieties of timothy and meadow fescue also sold out completely, and the outlook for production in Canada and Europe is very uncertain at this time.

The popularity of DLF’s market-leading varieties of Ryegrass PLUS and Tall Fescue PLUS raised consumption of festulolium to a new record. Sales growth was supported by customer adaptations of webinars from DLF’s marketing and product management team.

The popularity of DLF’s market-leading varieties of Ryegrass PLUS and Tall Fescue PLUS raised consumption of festulolium to a new record. Sales growth was supported by customer adaptations of webinars from DLF’s marketing and product management team.

Customer webinars, developed during the pandemic, will remain a valued tool for customers to learn more about the ways in which our products make a difference.

A relatively low demand for Italian and annual ryegrasses in the summer/fall 2020 mainly reflects an absence of the severe droughts that affected previous years. Sufficient supply for this year’s summer consumption seems likely.

Recommended smooth-stalked meadow grass remains on a firm price level. A few of the varieties featured on various national lists are still available. At DLF we’re delighted to have our new variety, JANKA, listed, alongside CHESTER.

The market for cocksfoot is recovering from an oversupply. It will fall back into balance during the summer, mainly driven by demand from outside EU.

After a strong demand for all recommended varieties of perennial ryegrass, the market is set to change. Demand for the most valued varieties, such as the highly digestible DLF Fiber Energy varieties, is set to remain at a high level, while average varieties on national lists must find their way into the market. There is, however, a global shortage of cheap varieties of perennial ryegrass from suppliers such as Denmark, Germany, Poland and New Zealand. Strong demand for these types from the USA and China seems to be steady.

After a strong demand for all recommended varieties of perennial ryegrass, the market is set to change. Demand for the most valued varieties, such as the highly digestible DLF Fiber Energy varieties, is set to remain at a high level, while average varieties on national lists must find their way into the market. There is, however, a global shortage of cheap varieties of perennial ryegrass from suppliers such as Denmark, Germany, Poland and New Zealand. Strong demand for these types from the USA and China seems to be steady.

Clovers and alfalfa are generally in balance. While prices for red clover and white clover are firming slightly to reflect European production and a reduced supply of white clover from Oceania. Production of the most popular varieties of alfalfa still seems insufficient.

OUTLOOK: The worldwide harvest counts this year more than ever … longer term, competition for land use will lift prices

Overall stock levels across Europe at the end of June will again be very low. The harvest of 2021 will therefore play a major role in balancing supply and demand over the coming 12 to 18 months. DLF’s crop acreage for 2021 is at last year’s level, and we’re expecting an average yield. So we’re hoping for a better June after a long, cold and wet spring in Northern Europe. So far the fields of grasses and clovers are looking well with good vegetative growth. In the absence of winter damage and spring drought, we are now looking for some warm and dry weather to ensure the generative phase of the plants. We need, and are hoping for, a good 2021 harvest. However, we already know that it will be a late one. In Canada we’re expecting lower yields where , for example, timothy is experiencing very dry conditions after a bad establishment. And from Oregon we hear of a record dry March to May.

Looking further ahead, we are looking to mitigate shortages across the globe by contracting new grass production with farmers. However, the current high prices for agricultural commodities such as winter wheat and winter oilseed rape (typically grown on the same types of farm and field as grass seed) will give farmers competitive alternatives.

Senior advisor, Henning Otte Hansen of the Department of Food and Resource Economics at the University of Copenhagen, explains:

“Factors such as more import by China, bottlenecks in global logistics, and increased economic activity after the reopening after Covid-19 have put upward pressure on the agricultural commodity markets. Several countries have also increased their demand for agricultural products in order to secure larger stocks as a result of the market uncertainty.”

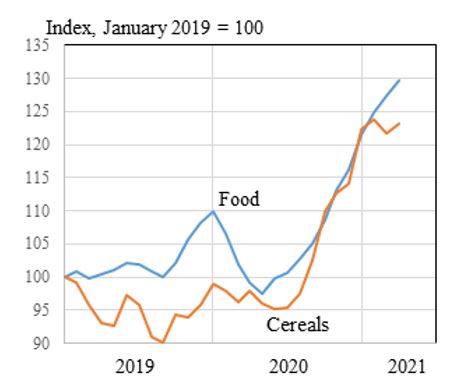

Global FAO price index: Food and cereals

According to Stefan Vogel, Head of Agri Commodity Markets Research and Global Sector Strategist, Grain & Oilseeds within Rabobank’s Food & Agribusiness Research, these are the key drivers for (multi-year) high agricultural commodity prices : weather related production issues, strong demand especially from China due to recovering hog sector, multi-year low inventories.

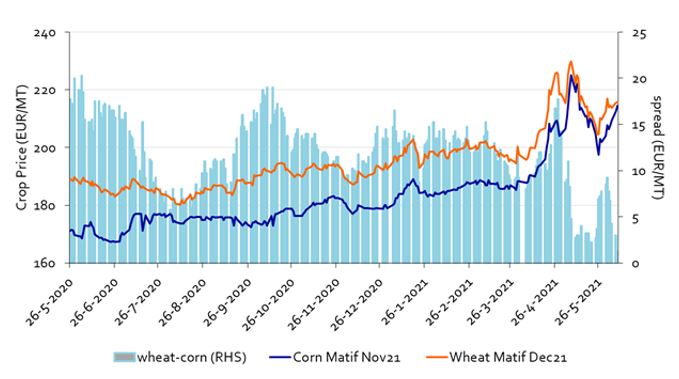

From below graph (source Bloomberg, Rabobank 2021) you can see that the pricing parity of wheat and corn pushes wheat up and makes wheat a follower of corn.

As a result farmers will ask for higher prices supported by guarantees for new grass-seed production.

Whatever happens in the world, one thing you can rely on is the support of your partner, DLF. Wherever you meet us, face-to-face or online, we will do our best to help you to cover your demand.